The day has come to make use of all those hard-earned dollars you’ve been saving and get a place of your own. For most of us, buying a property is a big undertaking, as homeownership comes with a hefty price tag and a long-term financial commitment.

It’s time to make some tough decisions. Do you want to put all that money in a resale flat? Or perhaps get a new launch condo instead? There are pros-n-cons to each, but in this guide, we will focus on the steps taken for buying a new launch condo.

These are the six steps you’ll need to familiarize yourself with for a successful New Launch Condo purchase.

Step 1: Financial Planning

Obtain the in-principle approval (IPA) from the financial institution

Buying a private property in Singapore is subject to an affordability assessment to determine your loan eligibility.

Total Debt Servicing Ratio (TDSR): This sets a limit on how much you can borrow from financial institutions (FI), who must ensure your monthly repayment for all debts (including mortgage, credit card bills, car loans, and personal loans) does not exceed 55% of your gross monthly income.

Loan-to-Value Ratio (LTV): Your LTV limit is up to 75% for your first housing loan. You’d need to cover the difference out of your pocket if you purchase a unit above valuation.

The IPA will be based on your financial capabilities and credit history and may take 7-30 days depending on the financial institution, the accuracy of the information you’ve provided, and whether you’ve submitted all the necessary documents.

Step 2: Shortlisting

Begin your home search

Research on property platforms such as TopHomes.sg by shortlisting the units that match your criteria and needs, from location, lifestyle, budget, the form of ownership (Leasehold/Freehold), and the property size.

As it can be time-consuming and a little bit overwhelming. This will be an excellent time to engage with a Realtor (such as myself) to help you through this process.

Step 3: Viewings

House Shopping

Perhaps the most exciting part of the process is viewing those shortlisted properties and getting ready to commit to your dream home.

At this stage, your agent (me) will be able to advise you on stock availability and any ongoing promotion, which would be the best stack/units which will meet your criteria.

Step 4: Booking

The actual purchase has started.

At the showflat, upon finalizing your unit of choice. The Developer with issue an Option To Purchase (OTP) and Property Details Information (PDI) form, which will contain everything you’ll need to know about the property.

More on the eight weeks payment schedule from OTP to completion is below.

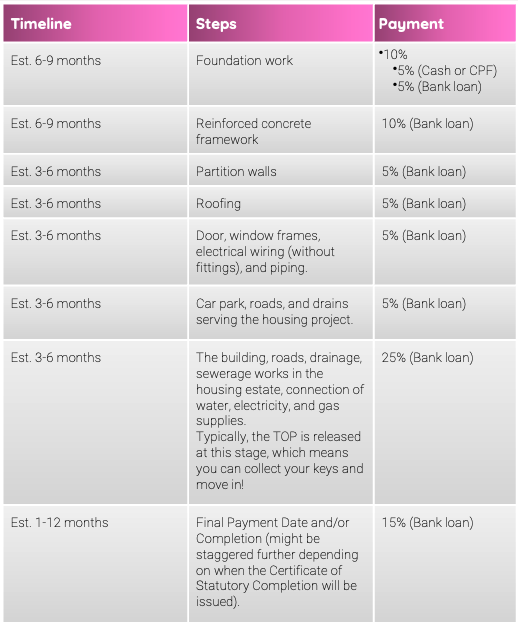

Step 5: Construction Phase

Progressive Payment Scheme

How much you’ll need to pay in addition to the OTP, S&P, and buyer stamp duties depends on when in the construction phase you have made your purchase. Ultimately there are eight payment schedules as per below:

1. Foundation: 10% (5% CPF or Cash and 5% Loan) 2. Framework: 10% (Loan can be used from here onwards) 3. Wall: 5% (of your unit) 4. Ceiling: 5% (of your unit) 5. Windows: 5% (of your unit) 6. Car Park: 5% 7. Temporary Occupation Permit (TOP): 25% 8. Legal Completion (CSC): 15% – 1 year after TOP

Receiving a Notice of Vacant Possession (NVP) from your Developer is an exciting part of your property journey.

With the hassle of endless financial documents, the joy and heartbreak of house hunting, and the potential wait for a property to be completed, you’re finally ready to take ownership of your home.

From this joyful moment onwards, for a period of 12 months, the Developer will provide a defect liability period before collecting the final payment known as the Legal Completion.

8 Weeks Payment Schedule

As mentioned above, an eight-week completion timeline will kick in once you sign the OTP and book your apartment.

8 Weeks Payment Schedule

On Issuance of the Option to Purchase (OTP) – 5% will be paid in cash by you.

Within the next two weeks, you’ll be appointing a conveyancing law firm to handle the proceedings on your behalf and start researching and applying for a bank loan. The Developer will issue three sets of the Sales & Purchase (S&P) agreements.

Once you’ve received your S&P, you’ll have three weeks to sign and submit all the documents and payments required to exercise the S&P successfully.

Finally, you’ll pay the 15% downpayment in Cash or CPF and proceed into the progressive payment scheme.

Progressive Payment Scheme

Here is a more detailed view of the Progressive Payment Scheme:

Progressive Payment Scheme

Overall you would be looking at a 3-4 years period for your new home to be built. If you still have questions I’ll be happy to further discuss this with you.

Hudson Place Residences recorded strong launch sales, but the bigger story may be what buyer demand is saying about Media Circle itself. This review looks at pricing, launch response, one-north positioning and whether buyers are moving into the district ahead of its residential transformation.

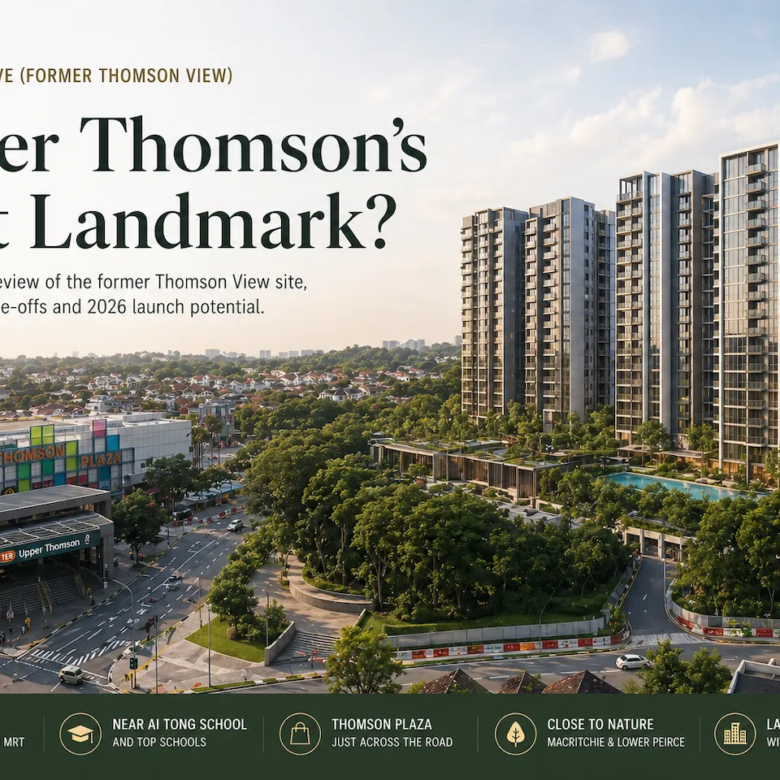

Thomson Reserve (formerly Thomson View) has many ingredients of a major 2026 launch: rare Upper Thomson scale, Ai Tong proximity, MRT convenience, Thomson Plaza, nature access, and likely mega-development ambition. But while the district already appears structurally strong, buyers may still need to assess whether Thomson Reserve’s eventual pricing reflects genuine long-term value — or simply one of 2026’s strongest launch narratives.

Vela Bay is an upcoming Bayshore condo in District 15. This review breaks down its location, pricing, layouts, and whether it’s a project worth considering for buyers.